New Schedules K-2 and K-3 (Form 1065) have been created by the IRS to offer standardized reporting of U.S. international tax information. The new formats include specific parts and boxes for certain items of international transactions, including withholding details and sourcing details. They will be used by partnerships and large corporations to report a wide range of business activities. That means many companies are now subject to more complex reporting requirements.

Regardless of the changes, the new Schedules will present additional challenges for international funds. The increased detail may create tax compliance burdens for funds and complicate investor-relations issues. Additionally, it could cause delays in the delivery of investor tax packages. Thus, funds and partnerships may need to review the timeline for preparing and delivering these documents.

For example, partnerships may need to separate the delivery of their Schedules K-1 from the delivery of their partner’s tax package. This could lead to a significant increase in compliance costs. And it may also force managers to revise timelines for delivering investor tax packages.

Why are the new forms needed?

The new forms were created to reduce confusion on the Schedule K. In the past, Schedule K and K-1 did not require specific formatting, which caused confusion. The new forms help to reduce confusion, inconsistent reporting, and inquiries by providing reporting consistency and clarity while enabling the IRS to “verify [that] partnership and S Corp items are properly reported on partners’ and shareholders’ returns.”

In the past, there was confusion about what to report and where to report it on the Schedule K and K-1 in relation to pass-through, partners and partnerships, shareholders, and S corporation’s income.

What else do the new schedules provide?

In addition to simplifying the filing process, the new schedules:

- Provide detailed information about sourcing for flow-through investors and partners.

- Clarify responsibilities and standardize reporting formats.

- Supply detailed information on sourcing and foreign-derived intangible income.

How does it impact my business?

For small and medium-sized businesses, the new regulations will require them to use software that automates and streamlines the filing process.

For larger businesses, the new Schedules contain comprehensive information on sourcing and other foreign-derived intangible income. For partnerships and S corporations, the new Schedules will add a major reporting requirement.

These forms will also require deep knowledge of complex international tax concepts, such as:

- Sourcing rules;

- Passive foreign investment companies, and;

- The GILTI rules.

The forms may be filed electrically, however, all the forms are not available as of yet. If you electronically file your return before the form release dates, submit your schedules as separate PDF files attached to the return.

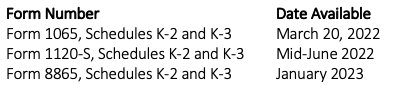

Form Release Dates

The filing of a full Schedule K-2 and K-3 is essential for companies of any size. Due to the new requirements, businesses need to file accurate and complete forms.

I don’t have any foreign activities or partners. Do I still need to file these forms?

In many instances, a partnership or S corporation with no foreign partners, foreign source income, no assets generating foreign source income, and no foreign taxes paid or accrued may still need to report information on Schedules K-2 and K-3. For example, if the partner or shareholder claims the foreign tax credit, the partner generally needs certain information from the partnership on Schedule K-3, Parts II and III, to complete Form 1116. Read the IRS’ FAQ #11 for more details on why and when you might need to complete these forms.

What if I submit incorrect forms?

The IRS claims that “Taxpayers who make a good faith effort to comply with the new schedules for the tax year 2021 will not be assessed a penalty. A filer will not be subject to penalties if it made a good faith effort to determine whether it must file a part and how to complete a part if it determines it must file.”

The filing of a full Schedule K-2 and K-3 is essential for companies of any size. Due to the new requirements, businesses need to file accurate and complete forms.

This is one area you should not tackle on your own. Work with me to help you sort through the confusion. Contact me today.